Example Workflow

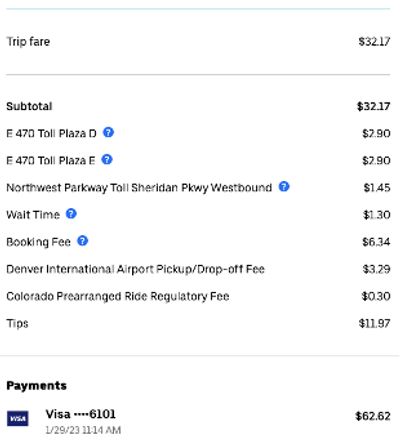

The Uber Receipt is a common and understandable workflow. In the example given to the right, we have a single credit card payment of $62.62 which is processed via a payment gateway. The Consumer gets out of the car thinking how simple it is to pay for a ride.

But then the problems begin. Uber must split that payment into many pieces and route these funds to the appropriate parties. For example, there may be multiple toll road operators which are paid by either a fleet operator or a gig driver. There is a wait time fee paid to the driver, but perhaps split with Uber. A booking fee is paid to Uber, but the airport also wants their fee. We must not forget the government, as they impose a regulatory fee. We then have the tip amount which must be handled separately of other funds, as the driver is responsible for paying income tax on this full amount. Not listed here is the payment processing fee and other hidden charges. Sales and VAT taxes must also be computed in many use cases.

Uber also allows the driver to receive their payment using a debit card, which involves interchange sharing between Uber and their bank. This introduces many more complexities.

There still remains the issue of reconciliation with payment gateways and issuing processors. We ideally submit each payment to fraud detection services, and move funds between settlement accounts and other bank accounts. Compliance and audit also come into play. The lists of responsibilities goes on, and on.

This is actually a simple money movement example, as eCommerce transactions involve partial authorizations, voids, partial returns, and more. Not all fees, of course, are actually refundable as the toll road operator and payment gateways will not return fees. Someone will be required to cover the shortfall when refunding a customer for a poor experience.

It is clear that building a money movement system is highly complex, and adds significant time, cost, and risk to any software development project. It would be better if a money movement service would just take care of all these complexities via simple configurations, and do it all in real time with all parties receiving funds in virtual accounts with optional auto-dispersal rules.

This "Money Movement as a Service" (MMaaS) is the motivation for Money Fabric.

How Money Fabric Solves for the Workflow Issue

Facilitating Roles

Facilitating Roles

Facilitating Roles

A facilitating role is any type of organization or user expecting to be paid, or required to pay, fees. Examples include Uber drivers, toll road operators, airports, etc.

With Money Fabric, you just define as many roles as you wish.

Business Processes

Facilitating Roles

Facilitating Roles

A Money Movement Process, or Workflow, defines how funds are distributes in response to a specific event. One example would be paying for an Uber ride. Each process has many facilitating roles.

With Money Fabric, you define as many processes as you wish.

Fee Rules

Facilitating Roles

Fee Rules

Fees are applied to facilitating parties based upon role, tender type, fee plan, and other parameters. Fees are applied in real-time, as business processes are executed.

Facilitating parties will have virtual accounts debited and credited in real time, when executing a process.

Pre-Built Integrations

Money Movement Processes, or Workflows, is just half of the equation when it comes to building a money movement system. Also included are a broad number of technical integrations which add signification costs to any project.

Payment Gateway

The payment gateway is responsible for processing the pay-ins and pay-outs using ACH, Credit Cards, or a variety of other tender types. This is not terribly complex for credit cards, but integrating with such alternative tender types as Venmo, Alipay, Cash App, etc can be daunting.

Issuing Processors

Debit card processing against virtual accounts requires a sophisticated ISO8583 integration to an issuing processor, bank, and program manager. This is a daunting challenge which Money Fabric has solved.

Core Banking

Moving funds between bank accounts is necessary for settlement, net interest income generation, and more. Gaining access to core banking APIs is difficult, much less performing the actual integration and issuing accurate transfer instructions.

Fraud Surveillance

You will be compelled to submit each pay-in and pay-out to a fraud surveillance platform for purpose of detecting fraudulent transactions. This is an expensive proposition which imposes hefty monthly minimum fees. Money Fabric is able to distribute this cost across multiple customers, therefore making this affordable.

Accounts Payable / Accounts Receivable

A money movement system must ultimately integrate to third party accounting systems, giving the organization a complete view of their financial position. We currently provide batch file integrations, and will work with customers on real-time API integrations.

Point of Sale

The Money Fabric team did build the Global Payments Vital Point of Sale system, as well as a bluetooth-enabled fob for embedding in unattended payment devices (such as laundry machines and vending machines).

We also have relationships with popular POS manufacturers, and can pursue enhancements to these POS devices for purpose of processing stored value transactions against Money Fabric virtual accounts.

Conclusion

Most businesses are not experts with either payments or money movement. They are, however, experts in ride sharing, logistics, sporting events, car dealerships, and more. It is wasteful for these firms to build expensive money movement development organizations, as that money is better spent on providing a better customer experience.

We have seen above that building a custom money movement solution is terribly difficult and highly expensive. Building ledgers, performing integrations, reversing transactions, and many other tasks will actually make many projects just unaffordable.

Money Fabric is a "Money Movement as a Service" which can essentially eliminate the complexities of building a money movement solution, and get you to market with significantly lower time, cost, and risk.